20 States Where College Is Worth the Cost

Every prospective student wonders: Is college worth it? One reliable way to measure that is by looking at the college’s return on investment (ROI).

To do this, students can compare the cost of their degrees (investment) to how much they’re able to earn upon graduating (return). While that investment typically includes taking out student loans — meaning you would graduate with debt — don’t fret too much. A recent study from LendingTree revealed that, generally, a college degree still pays off for most students.

But the exact value of a college degree as an investment — and the return of a higher salary — vary depending on where you live. Here are the top 20 states where college is a solid bet, as identified by the ROI of a bachelor’s degree in each state.

Top 20 states where college pays off

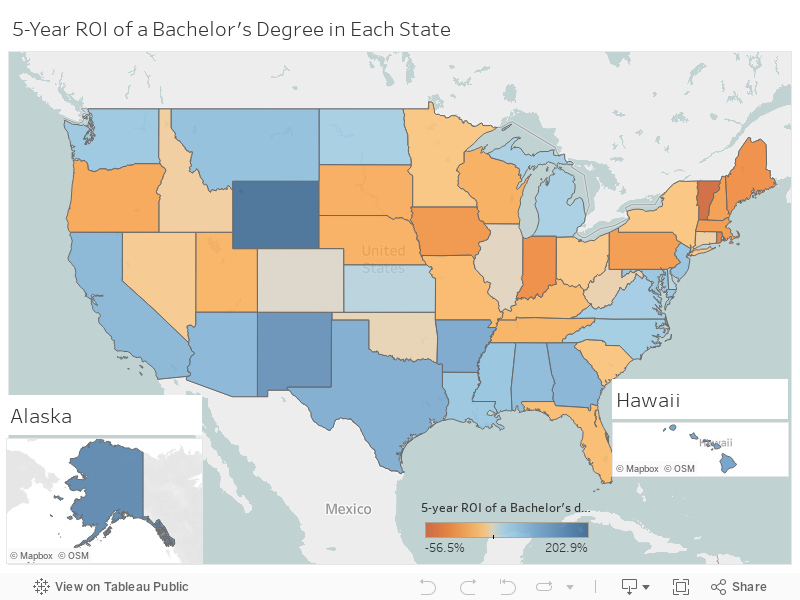

LendingTree calculated each state’s average return on investment of a college degree five years after graduation. This was done by finding the typical pay difference between workers in that state with a high school diploma versus a bachelor’s degree, then using state-specific college costs to calculate the ROI.

Overall, college proves to be a good bet for most students. A typical college grad will break even on college costs in about 3.7 years, and see an average pay bump of around $19,400.

What’s more, five years post-graduation, an average graduate’s ROI is just about 52%.

Of course, many states can yield a much better deal for college students. Here are the states in which a college degree is a smart investment, based on a five-year ROI.

1. Wyoming: 203% 5-year ROI on College

- Average high school graduate salary: $31,936

- Average bachelor’s degree holder salary: $45,519

- Increase in annual pay for earning a bachelor’s: $13,583

Wyoming has some of the highest wages for high school graduates: $31,936 a year, on average. This results in a 43 percent increase in pay for earning a bachelor’s degree.

College is a bargain in this state, too: A bachelor’s degree totals just $22,422 on average, the cheapest in the nation. With these low costs, a degree is a sound investment for Wyoming residents. A graduate will break even in 1.7 years, plus triple their initial investment within five years of graduating.

2. New Mexico: 151% 5-Year ROI on College

- Average high school graduate salary: $25,747

- Average bachelor’s degree holder salary: $43,257

- Increase in annual pay for earning a bachelor’s: $17,510

New Mexico workers with only a high school diploma are among some of the lowest-paid in the nation, earning $25,747 a year on average. However, wages for New Mexico college graduates also rank among the bottom 10 states in the nation.

Earning a bachelor’s results in a respectable 68 percent pay increase. And with the third-lowest college costs in the nation, at $34,945 for a bachelor’s degree, this investment pays off in only two years.

3. Arkansas: 120% 5-Year ROI on College

- Average high school graduate salary: $25,767

- Average bachelor’s degree holder salary: $44,101

- Increase in annual pay for earning a bachelor’s: $18,334

Average wages are also low for Arkansas’s high school grads; they earn $25,767 a year.

Yet someone with a bachelor’s degree earns an average income of $44,101 — that’s a 71 percent increase in pay.

Combine this impressive increase with low college costs of $41,629 for a four-year degree, and it takes just 2.3 years for the average grad to break even.

4. Texas: 114% 5-Year ROI on College

- Average high school graduate salary: $27,232

- Average bachelor’s degree holder salary: $51,701

- Increase in annual pay for earning a bachelor’s: $24,469

In Texas, earning a bachelor’s degree will generate an average pay increase of 90 percent — the third-highest in the nation.

This steep increase in pay means that college pays off for Texas residents. While that $57,121 price tag for a bachelor’s degree may be steep, college grads will break even in 2.3 years.

5. Georgia: 105% 5-Year ROI on College

- Average high school graduate salary: $26,350

- Average bachelor’s degree holder salary: $49,989

- Increase in annual pay for earning a bachelor’s: $23,639

Workers in Georgia who attain a bachelor’s degree earn 90 percent more than those with just a high school diploma. This means attending college can nearly double pay for most residents in this state.

Combine this big pay boost with lower college costs, and grads can quickly earn back the investment of a college degree in 2.4 years.

6. Arizona: 102% 5-Year ROI on College

- Average high school graduate salary: $26,898

- Average bachelor’s degree holder salary: $48,159

- Increase in annual pay for earning a bachelor’s: $21,261

A typical Arizona resident will break even on college costs in only 2.5 years. That’s thanks to the low costs of a bachelor’s degree, at $52,524. It also reflects a higher local pay difference of 79 percent from high school to college levels of educational attainment.

7. California: 102% 5-Year ROI on College

- Average high school graduate salary: $27,963

- Average bachelor’s degree holder salary: $56,010

- Increase in annual pay for earning a bachelor’s: $28,047

California’s jump in pay from a high school to an undergraduate diploma is the second-highest among the top 20 states listed in this study. The average pay for workers with bachelor’s degrees is, in fact, more than double what high school graduates earn in this state.

At 102 percent, that’s the biggest pay increase for earning a bachelor’s degree in any state. That helps college graduates earn back the investment of a degree in 2.5 years.

8. Alabama: 96% 5-Year ROI on College

- Average high school graduate salary: $26,132

- Average bachelor’s degree holder salary: $46,434

- Increase in annual pay for earning a bachelor’s: $20,302

The pay levels for Alabama college graduates are about 78 percent higher than high school grads in this state. Thanks to this percentage, residents with bachelor’s degrees break even on the $51,732 cost of a degree in 2.6 years.

9. Alaska: 95% 5-Year ROI on College

- Average high school graduate salary: $34,236

- Average bachelor’s degree holder salary: $52,769

- Increase in annual pay for earning a bachelor’s: $18,560

Alaska’s high school graduates are the best paid in the U.S., earning $34,236 on average.

What’s more, the average salary for a college graduate in Alaska is 54 percent higher than graduates who only hold a high school diploma, a smaller gap than in most states.

However, residents of this state receive a relatively low-cost education at $47,524 in this state, and break even in just 2.6 years.

10. Montana: 92% 5-Year ROI on College

- Average high school graduate salary: $25,186

- Average bachelor’s degree holder salary: $38,283

- Increase in annual pay for earning a bachelor’s: $13,097

Montana has some of the lowest college costs in the country. In fact, a bachelor’s degree costs just $34,184, an investment a college grad in this state will earn back in just 2.6 years.

However, Montana is actually the lowest-paying state for college graduates. It’s also the only place where a bachelor’s degree doesn’t come with an average pay greater than $40,000 a year. Overall, a bachelor’s degree only bumps up annual pay by 52 percent.

11. New Jersey: 85% 5-Year ROI on College

- Average high school graduate salary: $32,207

- Average bachelor’s degree holder salary: $61,128

- Increase in annual pay for earning a bachelor’s: $28,921

Among these 20 top states, New Jersey has the highest incomes for graduates with a bachelor’s and the highest dollar-for-dollar pay increase from high school diploma to a bachelor’s degree (a bump of 90 percent).

This makes college a good deal, even with the state’s higher college costs — a bachelor’s degree costs just over $78,000. But New Jersey college grads can recoup that cost in 2.7 years, thanks to the state’s higher incomes.

12. Mississippi: 84% 5-Year ROI on College

- Average high school graduate salary: $25,954

- Average bachelor’s degree holder salary: $40,952

- Increase in annual pay for earning a bachelor’s: $14,998

Mississippi is another state in which wages start low for those with high school diplomas.

However, wages for college graduates are also among the lowest of any state ranked among the top 20. Unfortunately, that means a graduate with a bachelor’s degree will only see a pay increase of 58 percent — a pay bump that lags behind college graduates in most other states.

The low cost of college in Mississippi means college still pays off in this state. The typical college grad will break even in 2.7 years.

13. Maryland: 82% 5-Year ROI on College

- Average high school graduate salary: $33,584

- Average bachelor’s degree holder salary: $60,287

- Increase in annual pay for earning a bachelor’s: $26,703

Maryland is the only other top 20 state (besides New Jersey) in which bachelor’s graduates earn more than $60,000 a year.

In fact, those with a high school diploma can expect an average pay increase of 80 percent after earning a bachelor’s degree. This means that with a steeper-than-average cost of a bachelor’s degree of $73,213, most graduates will break even in 2.7 years.

14. Louisiana: 81% 5-Year ROI on College

- Average high school graduate salary: $28,300

- Average bachelor’s degree holder salary: $47,115

- Increase in annual pay for earning a bachelor’s: $18,815

In Louisiana, a bachelor’s degree typically results in a 66 percent boost in pay, putting this state near the middle of the pack in this measure. However, lower costs on college mean a typical grad needs only 2.8 years to repay the average $51,973 bachelor’s degree.

15. Washington: 80% 5-Year ROI on College

- Average high school graduate salary: $31,011

- Average bachelor’s degree holder salary: $53,802

- Increase in annual pay for earning a bachelor’s: $22,791

Washington residents can earn a bachelor’s degree at an average cost of $63,281, and break even on this cost in 2.8 years. The higher dollar difference in average pay between the state’s high school and college grads represents a 73 percent increase for the latter.

16. Hawaii: 75% 5-Year ROI on College

- Average high school graduate salary: $30,971

- Average bachelor’s degree holder salary: $46,590

- Increase in annual pay for earning a bachelor’s: $15,619

In Hawaii, earning a bachelor’s degree results in an average pay increase of 50 percent — one of the lowest (by percentage difference) in the nation.

However, the relatively low cost of $44,738 of a bachelor’s degree in this state makes for a smart investment. Plus, a typical college graduate will earn back the money spent on a degree in a short 2.9 years.

17. Virginia: 72% 5-Year ROI on College

- Average high school graduate salary: $29,303

- Average bachelor’s degree holder salary: $55,509

- Increase in annual pay for earning a bachelor’s: $26,206

Earning a bachelor’s degree is an achievement worth an 89 percent pay bump in Virginia, one of the largest pay increases in the nation. These higher earnings mean the average Virginia college graduate can pay back his or her $76,000 bachelor’s degree in 2.9 years.

18. North Carolina: 71% 5-Year ROI on College

- Average high school graduate salary: $26,059

- Average bachelor’s degree holder salary: $45,377

- Increase in annual pay for earning a bachelor’s: $19,318

College costs are lower than average among North Carolina colleges at $56,400 for a four-year degree.

What’s more, this cost is recouped in just 2.9 years. That’s thanks to the decent jump in pay for North Carolina residents with bachelor’s degrees, who earn 74 percent more than workers with only a high school diploma.

19. North Dakota: 69% 5-Year ROI on College

- Average high school graduate salary: $31,691

- Average bachelor’s degree holder salary: $43,555

- Increase in annual pay for earning a bachelor’s: $11,864

North Dakota has the lowest-percentage pay bump from earning a bachelor’s degree in the nation — only 37 percent. That’s largely because high school graduates earn higher wages, with North Dakota among the 10 states that pay these workers the most.

Despite having one of the smallest gaps in pay between these two educational degree levels, North Dakota residents would still benefit from the state’s low college costs. A $35,198 price tag for a bachelor’s degree is the fourth-lowest in the nation.

College graduates would break even on these costs after three years.

20. Michigan: 66% 5-Year ROI on College

- Average high school graduate salary: $26,347

- Average bachelor’s degree holder salary: $48,622

- Increase in annual pay for earning a bachelor’s: $22,275

Last on the list is Michigan, a state that earns its spot thanks to the higher pay of college graduates. Michigan workers with a bachelor’s degree earn 85 percent more, on average, than those with high school diplomas.

With such a big pay bump, graduates break even on the $67,130 cost of a four-year degree in three years.

Methodology

LendingTree sourced wage data by state and educational attainment from the U.S. Census Bureau.

College costs were based on data from a previous LendingTree study finding the average cost of a college credit in each state, multiplied by the typical 120 credit hours required for a bachelor’s degree.

Return on investment data was calculated by finding the differences in average wages between a high school graduate and a worker with a bachelor’s degree in a given state, multiplied over five years. This was then compared to the initial cost of a bachelor’s degree in that state by calculating the five-year ROI.

| Rank | State | High school graduate salary | College graduate salary | Pay difference with college degree | Cost of a Bachelor’s degree | 5-year ROI of a Bachelor’s degree | Years to break even on college costs |

|---|---|---|---|---|---|---|---|

| 1 | Wyoming | $31,936 | $45,519 | $13,583 | $22,422 | 202.89% | 1.65 |

| 2 | New Mexico | $25,747 | $43,257 | $17,510 | $34,945 | 150.54% | 2.00 |

| 3 | Arkansas | $25,767 | $44,101 | $18,334 | $41,629 | 120.21% | 2.27 |

| 4 | Texas | $27,232 | $51,701 | $24,469 | $57,121 | 114.18% | 2.33 |

| 5 | Georgia | $26,350 | $49,989 | $23,639 | $57,719 | 104.78% | 2.44 |

| 6 | Arizona | $26,898 | $48,159 | $21,261 | $52,524 | 102.39% | 2.47 |

| 7 | California | $27,963 | $56,010 | $28,047 | $69,506 | 101.76% | 2.48 |

| 8 | Alabama | $26,132 | $46,434 | $20,302 | $51,732 | 96.22% | 2.55 |

| 9 | Alaska | $34,236 | $52,769 | $18,533 | $47,524 | 94.99% | 2.56 |

| 10 | Montana | $25,186 | $38,283 | $13,097 | $34,184 | 91.56% | 2.61 |

| 11 | New Jersey | $32,207 | $61,128 | $28,921 | $78,100 | 85.15% | 2.70 |

| 12 | Mississippi | $25,954 | $40,952 | $14,998 | $40,657 | 84.44% | 2.71 |

| 13 | Maryland | $33,584 | $60,287 | $26,703 | $73,213 | 82.36% | 2.74 |

| 14 | Louisiana | $28,300 | $47,115 | $18,815 | $51,973 | 81.01% | 2.76 |

| 15 | Washington | $31,011 | $53,802 | $22,791 | $63,281 | 80.08% | 2.78 |

| 16 | Hawaii | $30,971 | $46,590 | $15,619 | $44,738 | 74.56% | 2.86 |

| 17 | Virginia | $29,303 | $55,509 | $26,206 | $75,970 | 72.48% | 2.90 |

| 18 | North Carolina | $26,059 | $45,377 | $19,318 | $56,410 | 71.23% | 2.92 |

| 19 | North Dakota | $31,691 | $43,555 | $11,864 | $35,198 | 68.53% | 2.97 |

| 20 | Michigan | $26,347 | $48,622 | $22,275 | $67,130 | 65.91% | 3.01 |

| 21 | Delaware | $30,981 | $51,156 | $20,175 | $62,078 | 62.50% | 3.08 |

| 22 | Kansas | $27,716 | $45,639 | $17,923 | $55,448 | 61.62% | 3.09 |

| 23 | Colorado | $30,366 | $48,901 | $18,535 | $61,226 | 51.36% | 3.30 |

| 24 | Illinois | $28,850 | $52,080 | $23,230 | $77,702 | 49.48% | 3.34 |

| 25 | District of Columbia | $29,756 | $62,267 | $32,511 | $110,050 | 47.71% | 3.38 |

| 26 | Oklahoma | $27,001 | $42,732 | $15,731 | $53,429 | 47.21% | 3.40 |

| 27 | West Virginia | $26,844 | $42,183 | $15,339 | $52,474 | 46.16% | 3.42 |

| 28 | Connecticut | $33,775 | $60,338 | $26,563 | $92,028 | 44.32% | 3.46 |

| 29 | Idaho | $25,140 | $40,843 | $15,703 | $54,868 | 43.10% | 3.49 |

| 30 | Nevada | $29,351 | $45,840 | $16,489 | $58,660 | 40.55% | 3.56 |

| 31 | Ohio | $28,203 | $49,281 | $21,078 | $75,800 | 39.04% | 3.60 |

| 32 | Minnesota | $30,662 | $51,329 | $20,667 | $75,272 | 37.28% | 3.64 |

| 33 | New York | $30,084 | $54,214 | $24,130 | $88,700 | 36.02% | 3.68 |

| 34 | South Carolina | $25,698 | $43,712 | $18,014 | $66,614 | 35.21% | 3.70 |

| 35 | Florida | $25,275 | $43,371 | $18,096 | $70,750 | 27.89% | 3.91 |

| 36 | Kentucky | $26,518 | $44,249 | $17,731 | $69,478 | 27.60% | 3.92 |

| 37 | Missouri | $27,162 | $44,482 | $17,320 | $68,875 | 25.73% | 3.98 |

| 38 | Utah | $29,531 | $45,046 | $15,515 | $64,316 | 20.61% | 4.15 |

| 39 | Tennessee | $25,990 | $44,289 | $18,299 | $76,297 | 19.92% | 4.17 |

| 40 | Nebraska | $28,325 | $44,255 | $15,930 | $67,895 | 17.31% | 4.26 |

| 41 | Wisconsin | $29,904 | $47,339 | $17,435 | $75,422 | 15.58% | 4.33 |

| 42 | South Dakota | $27,706 | $40,472 | $12,766 | $55,804 | 14.38% | 4.37 |

| 43 | Oregon | $26,514 | $43,452 | $16,938 | $77,652 | 9.06% | 4.58 |

| 44 | New Hampshire | $32,844 | $51,767 | $18,923 | $93,098 | 1.63% | 4.92 |

| 45 | Pennsylvania | $29,692 | $50,170 | $20,478 | $103,810 | -1.37% | 5.07 |

| 46 | Massachusetts | $32,237 | $57,029 | $24,792 | $126,338 | -1.88% | 5.10 |

| 47 | Iowa | $29,615 | $46,382 | $16,767 | $88,702 | -5.49% | 5.29 |

| 48 | Maine | $26,716 | $41,612 | $14,896 | $83,966 | -11.30% | 5.64 |

| 49 | Indiana | $28,846 | $45,632 | $16,786 | $96,182 | -12.74% | 5.73 |

| 50 | Rhode Island | $31,196 | $51,769 | $20,573 | $139,248 | -26.13% | 6.77 |

| 51 | Vermont | $29,566 | $41,109 | $11,543 | $132,793 | -56.54% | 11.50 |